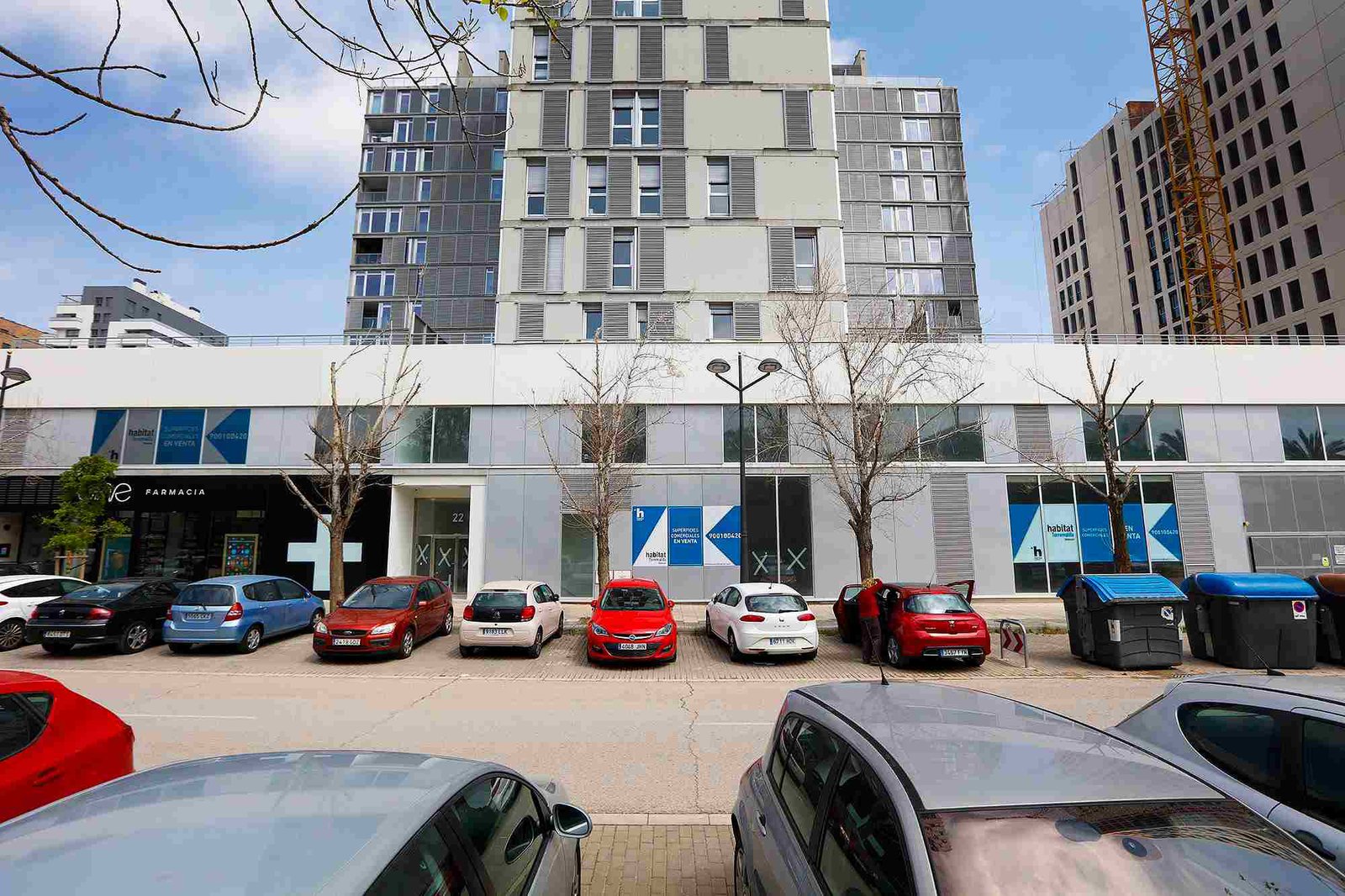

Last available comercial property. Immediate delivery.

Habitat Rio Segre Commercial Properties

Valencia, Valencia

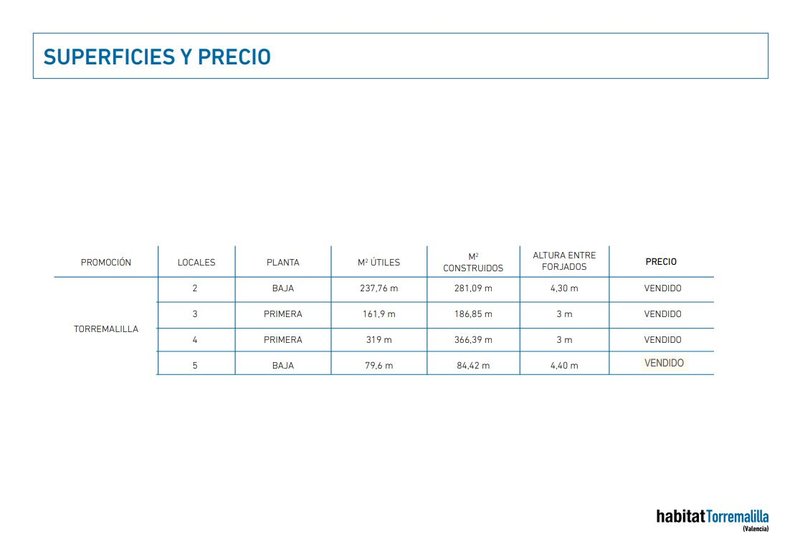

From

95.70 m2

From

161,000 €